|

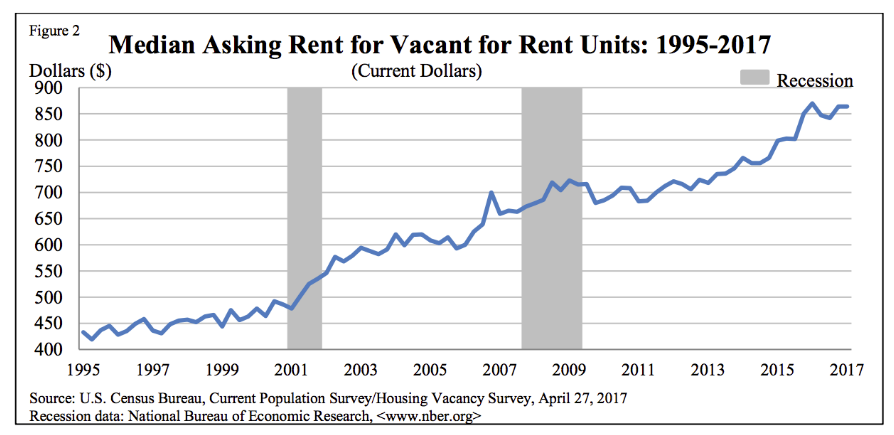

Most days, I listen to Marketplace on NPR. Their Divided Decade segments bring us stories on how the Great Recession has impacted us now that it has been 10 years since 2008. The pieces make me think about my home ownership story over the last 10 years and how the Great Recession impacted me and the conclusions that I have come to are that luck propelled me significantly through the recession and that increases in wealth have a compound effect that widen the gap between the rich and the poor. I generally consider myself a lucky person (and was fortunate enough to marry someone who also considers themselves lucky) and prescribe to Richard Wiseman's ideas on the topic. I graduated with a master's degree in biology in May of 2008 and started a job as a research scientist at a local university in August with an annual salary of $40,000. I was ecstatic. I could afford a fixer-upper in this affordable little neighborhood called West Asheville (NC) where my group of former raft guide friends went to grow up. With my dad cracking the whip, I went to the bank the day I got my job contract - a one page, single-sided mimeograph of degraded quality with my name, salary, and year-to-year basis written in by hand. You could never get a loan with that non-sense nowadays, but I applied for a loan at the end of the glory days. With no college debt (thanks, dad, for working at a college with tuition exchange), I got approved for more than I was comfortable paying (can you imagine?), but eventually settled on an 896 sq. ft. two bedroom one bathroom 1925 bungalow that needed some TLC. OK, it needed a new kitchen, bathroom, and some minor structural work, but the walls, floors, and roof would last for a little while longer. What? You don't like your knees hitting the tub when you sit on the toilet? So why do I mention luck? I closed on the house on September 18th, 2008. For those of you a little fuzzy on the chronology of 2008, Lehman Brothers failed the week before, or so. The image below shows the Dow Jones Industrial Average from 2008 - 2013 with September 18th highlighted by the vertical line. On a macro level, things were a little crazy and the collapse was beginning. On a micro level, the specifics of the house I had settled on were also crazy: the divorced owners of the house were living in the house, but not on speaking terms, rejected my original offer, and then countered. The house had been on the market for almost a year and with the economy tanking, I imagine their agent suggested taking what they could get. They had to sort out (in court) who had a right to the proceeds of the house. There were questions of the authenticity of some signatures on some of the documents and my agent even called me the morning of closing to say he didn't think it would happen. One of the owners was 30 minutes late. We all got settled into different rooms of the law firm and were shuttled in and out of different doors so none of us ever saw each others. I consider it dumb luck that it all worked out and I got the keys by noon. I didn't think the timing of my purchase was such a big deal at the time.  There are exceptions, but for many people (including me), the ability to purchase a house and hang onto it represents the biggest potential increase in personal wealth. Two of my family members declared bankruptcy during the recession due to underwater mortgages, lost their houses, and have only now begun to accumulate any significant wealth. My own parents were frighteningly close. I came home at Thanksgiving to visit my dad and stepmom who asked me at dinner, "What about the homeowner with an underwater mortgage? What should be done?" I was unforgiving: I said that it was their fault that they were living beyond their means and that they should have carefully calculated mortgage payments. My parents paused. My stepmom then asked, "What if someone had two underwater mortgages?" I understood that this was not hypothetical and I began to fret. My dad wanted to declare bankruptcy, but fortunately, my stepmom was able to talk him out of it. They had enough equity in the houses to use home equity lines of credit to pay bills for years while the economy improved and then sold at a profit. Their ability to hang onto the houses are what separated them from millions of others who were not. My parents aren't millionaires, but they are very comfortable in their retirement due to their optimism in the market. Another avenue through which those that hung onto houses were able to get richer was through accessory dwelling units or ADUs. I also chose this path, but out of need. Older houses have higher maintenance costs and on a single income, if the oil furnace died or the roof needed to be replaced, I didn't have a back-up fund. I took a gamble and decided to go $35,000 further into debt to build a 300 s.f. ADU. That's pretty cheap because I did a ton of the work myself and with my then girlfriend, now wife. Homeownership was a priority for me and I made some sacrifices: terrible roommates (not you, Susan!), no kitchen for 5 years, doing the home improvements myself, building the ADU, and on and on. But now others like me are much more likely to be considered middle or upper class. I would be remiss if I did not mention that after 7 years of solo home ownership, I married someone with a good job, thereby eliminating much financial stress, but I maintain my conclusions that homeowners accumulate wealth at a faster rate than others. Authors agree (here and here), but others do not. The compound effect of ownership on wealth is profound: since 2008, the Zillow Zestimate of the little house pictured above has doubled without considering the studio apartment. A 2 bedroom, 1 bath sub-1,000 s.f. house nearby just sold for $270,000. Appreciation is just one of the compound benefits. If I hadn't been able to keep the house, I couldn't have built the apartment. Homeownership drives the wealth gap and has widened the gap between the rich and the poor truly earning the name Divided Decade. Several of my friends in the original group that purchased around the recession have now upgraded houses, moving to larger houses while keeping the mortgage about the same time. They get richer when they do that. So what can be done? Urban land is no longer affordable. Rents are peaking. Asheville leads the U.S. in housing stock percentage taken by short term rentals (3%). My blog post on affordable land in Asheville is a microcosm of other cities and I presented my maps to the board of trustees of Habitat for Humanity. One Habitat home owner suggested capping sales prices of homes. I pointed out their idea might be met with stiff resistance from folks who have invested a lot in their homes. Other friends of mine who rent debate the merits of home ownership and the entire model. We must be in another bubble, right? My sad and anticlimactic answer to the question of what can be done is: I don't know. I really don't know, but I do care. Send me any thoughts you have. Thanks for reading!  Post Script/Funny Aside:

Another reason I consider both the purchase of a home in 2008 to be lucky and my continued ability to afford it to be lucky is that my job was grant funded. To fund my position, wealthy donors pledged over $100,000 to the university in early 2008 and I was hired and began to be paid based on that pledge, but when the economy tanked, the donors balked and never actually gave the full amount of money to the university. (This is actually more common than you might think because no university public relations office wants to run that story.) My boss elected to pay me using a different pot of money, but I have to think that the purchase of my house was a factor in his decision. I distinctly recall being in a work meeting with the office staff sometime in November 2018. My boss interrupted me to ask, "Did you buy a house?" I stared at him and blinked, "What?" He repeated the question, "Did you buy a house?" I said, "I don't think that has to do with work." He insisted and I told him I had. In retrospect, what could he do? Lay me off? He could have and I don't think I would have blamed him, but luckily, I stayed on for almost 6 years until (prompted by the lack of grant money) I left to pursue a Ph.D. (which is going swimmingly). If I hadn't been able to keep the job, I don't know if I would have been able to keep the house. |

etc.Of interest to me and hopefully at least one other person Archives

October 2019

Categories

All

|

RSS Feed

RSS Feed